Monopsony Power and the Transmission of Monetary Policy

Jan 1, 2025·, ·

0 min read

·

0 min read

Bence Bardoczy

Gideon Bornstein

Sergio Salgado

Abstract

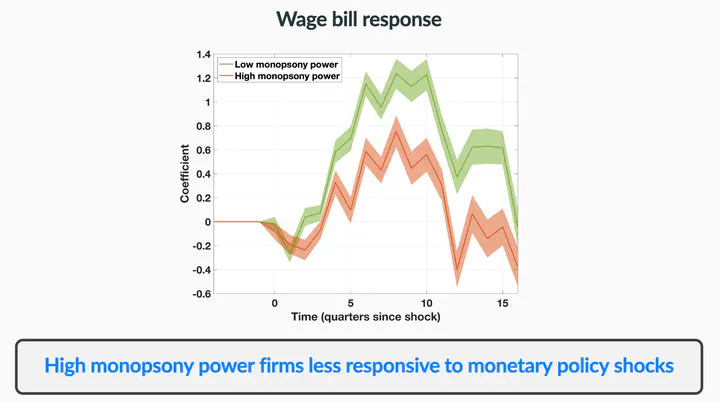

This paper studies how labor market power affects the efficacy of monetary policy. First, we use administrative U.S. Census data to document that firms with high monopsony power—firms who account for more than 10% of the wage bill in their local labor market—are less responsive to monetary policy in terms of their overall wage bill. Second, we construct a heterogeneous oligopsonistic New-Keynesian model to study how the decline in labor market power over the past four decades affected the transmission of monetary policy. We show that wage stickiness is key to obtain the heterogeneous response across firms. One contribution of our paper is to develop a numerical approach to solve the model. Such task is non-trivial as each local labor market consists of a finite number of firms, and a law-of-large numbers cannot be invoked to eliminate the local uncertainty resulting from wage stickiness. We calibrate the model to match key features of the U.S. labor market. We find that the decline in labor market power since the 1980s has amplified the aggregate effect of monetary policy on output by about 18%.