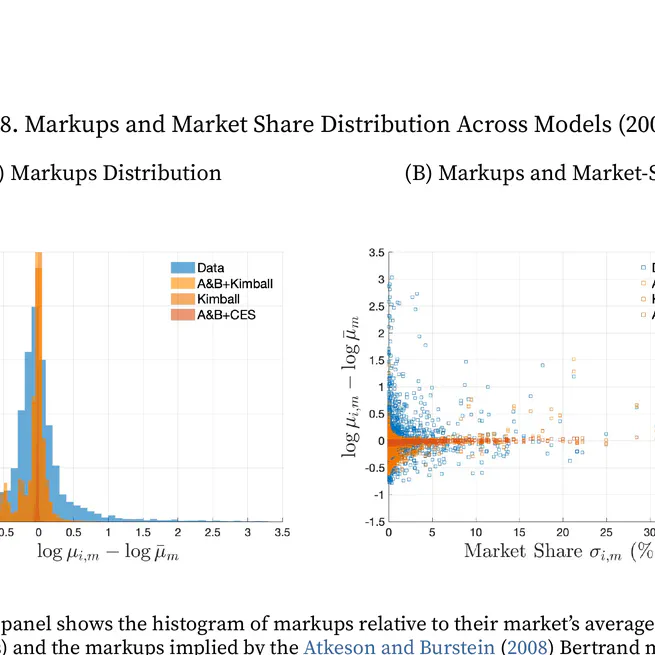

Markup Accounting

We document new facts of markup dispersion using firms in India, the US, and 10 European countries, and develop an oligopolistic model with demand elasticity shifters that accounts for the joint distribution of markups and firm size.

Jul 19, 2026

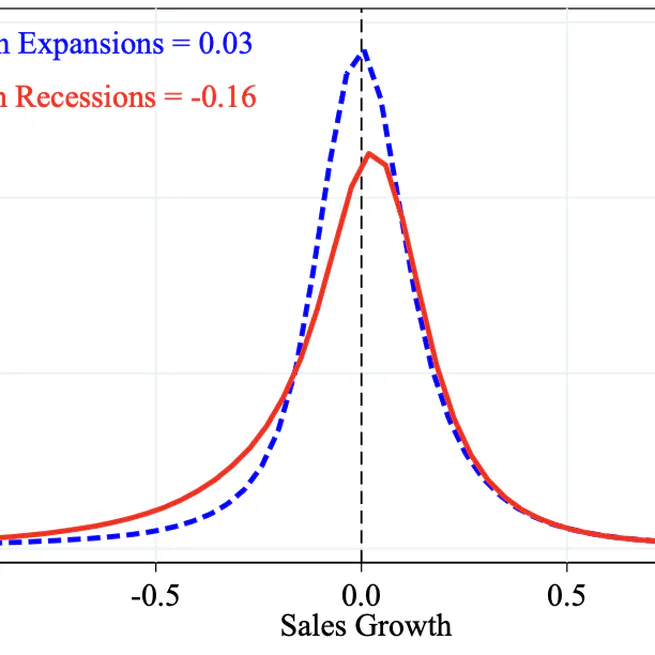

Skewed Business Cycles

We show that the skewness of firm-level growth rates is robustly procyclical across the U.S. and over 60 countries, and argue that recessions combine negative mean, positive uncertainty, and negative skewness shocks.

Jul 17, 2026

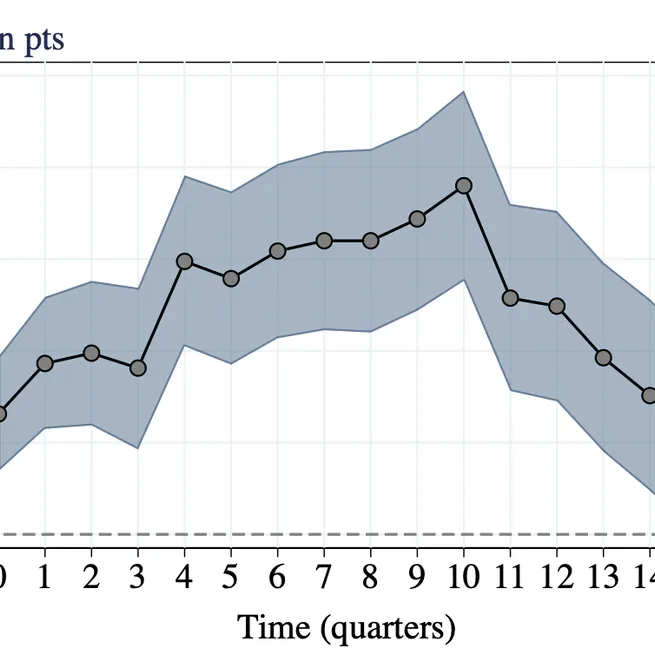

Monopsony Power and the Transmission of Monetary Policy

We show that firms with high monopsony power respond less to monetary policy and that the decline in labor market power since the 1980s has amplified the output effects of monetary policy.

Jun 5, 2026

Identifying Uncertainty, Learning about Productivity, and Human Capital Acquisition

We prove identification of labor market models with human capital acquisition, learning, and sorting, and show that differences in learning opportunities help explain low measured sorting despite high firm-worker complementarity.

Nov 1, 2025

Characterizing Income Risk in Chile and the Role of Labor Market Flows

We characterize Chilean income dynamics using 21 years of administrative data, finding declining inequality but rising volatility and negative skewness driven by within-job and between-employer earnings fluctuations.

Nov 1, 2025

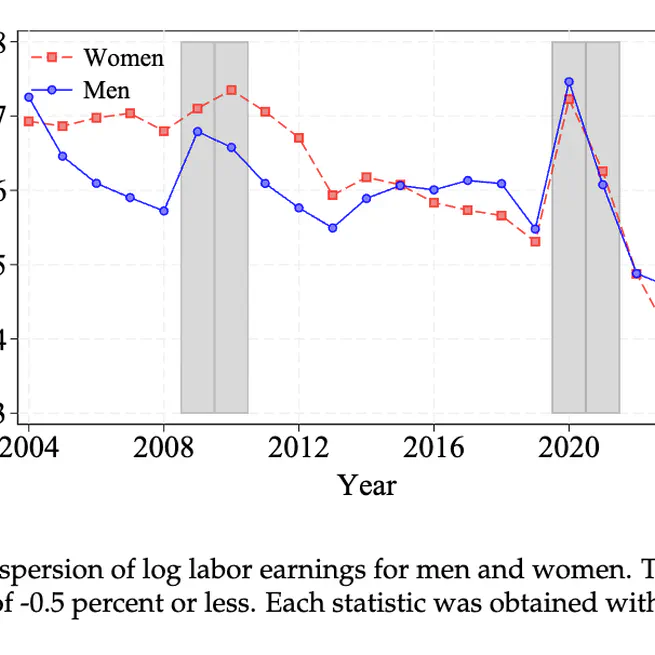

Are Minimum Wages and Income Taxes Complements or Substitutes in Addressing Rising Skill Premia?

We study the interaction between minimum wages and income taxes during rising wage inequality and show that their correlation is tied to skill premia, rationalized by a model with private productivity information.

Aug 28, 2025

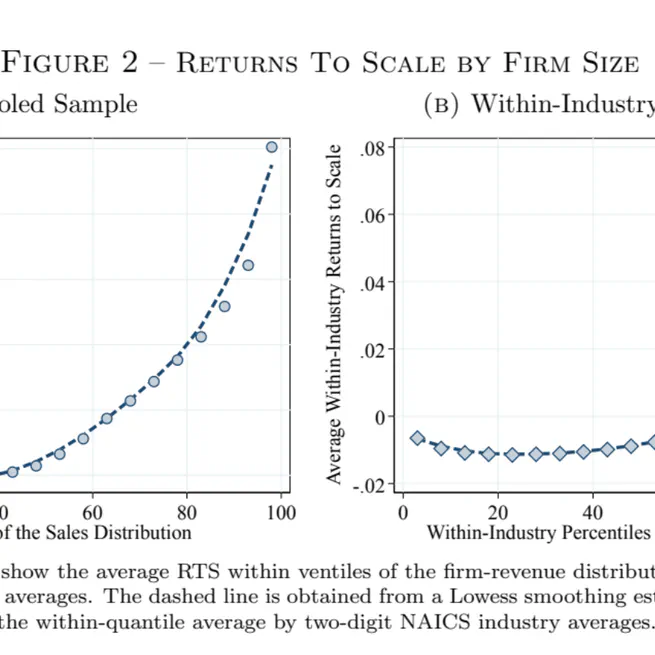

Scalable versus Productive Technologies

We disentangle returns to scale from TFP across firms and show that larger firms operate more scalable—but not necessarily more productive—technologies, amplifying efficiency losses from financial frictions.

May 6, 2025

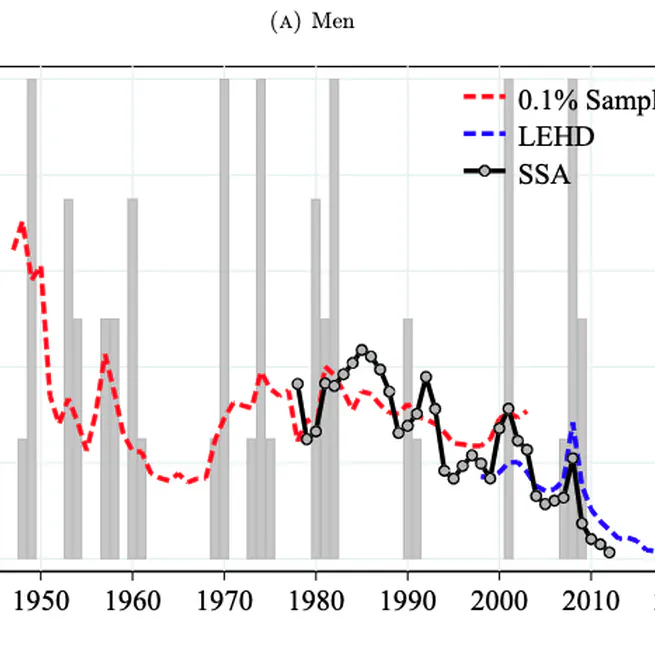

Evaluating the Great Micro Moderation

We show that U.S. worker income volatility has been stable or declining since the 1950s—contradicting survey-based beliefs—and link this trend to declining firm-side volatility.

Oct 25, 2023

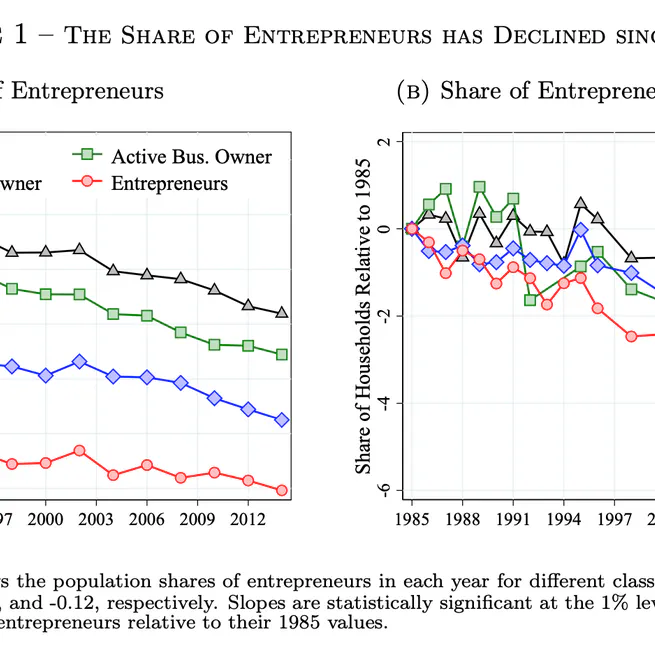

Technical Change and Entrepreneurship

I argue that skill-biased technical change and falling capital prices explain three-quarters of the decline in U.S. entrepreneurship by raising the returns to high-skill wage employment.

Jul 29, 2020